Dubai Commercial Rooftop Solar Potential

Dubai is no stranger to solar. Over the past decade, the Emirate has emerged as a regional leader in renewable energy adoption—backed by a clear regulatory framework, strong utility engagement, and a forward-looking energy vision.

Since the launch of Shams Dubai by Dubai Electricity and Water Authority (DEWA), the commercial and industrial (C&I) solar sector has flourished—with thousands of systems installed and a mature ecosystem of developers, EPCs, and consultants. The foundation is solid.

Yet even in this well-developed market, the Dubai commercial rooftop solar potential is still enormous. We scanned the rooftops—here’s what we found.

15,283

Total C&I Rooftops

5 GW

Total Solar Potential

5.6%

Solar Adoption

Why Dubai’s Rooftop Solar Market Matters

Dubai offers a unique mix of factors that make rooftop solar highly attractive: year-round sunlight, modern building infrastructure, and a clear regulatory environment.

DEWA’s Shams Dubai initiative—launched in 2015—paved the way for grid-connected rooftop solar, enabling net metering and streamlined approvals. Since then, the Emirate has built one of the most active solar rooftop markets in the Middle East.

As energy prices fluctuate and net-zero targets move closer, the pressure on businesses to take action is growing. And that’s where mid-sized rooftops become the next frontier.

What the Rooftop Solar Data Reveals

Dubai’s commercial and industrial building stock is large—and growing. With over 15,000 rooftops across the Emirate, there’s no shortage of surface area waiting to be activated for solar. When Planno analyzed the data, it became clear that the city’s solar potential remains largely underutilized despite a decade of regulatory support and market maturity.

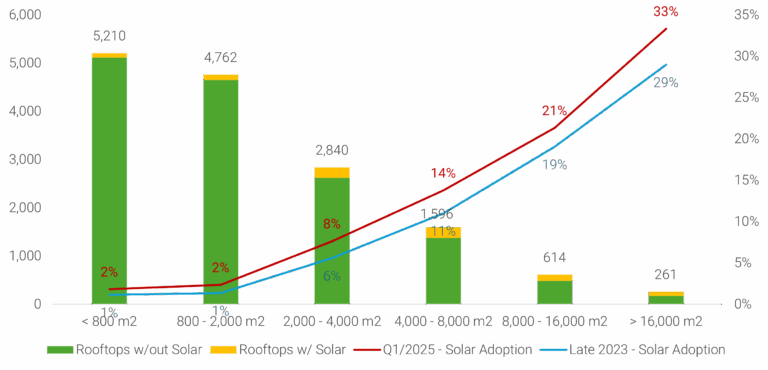

The rooftops identified range widely in size, from small logistics buildings to large-scale industrial facilities. Yet what stands out most is that more than 94% of these rooftops have yet to adopt solar, leaving over 4 GWp of potential still on the table.

Interestingly, the largest concentration of untapped opportunity lies not in the extreme ends of the market, but in the middle. Rooftops between 2,000 and 8,000 m² account for the bulk of surface area and represent the most promising segment for growth. These buildings are typically easier to permit and faster to develop than very large sites, while still offering solid economies of scale.

The distribution skews toward smaller mid-sized assets, with over 7,600 rooftops falling into the 800 to 4,000 m² category alone. These are the types of buildings found in Dubai’s many industrial parks, warehouse districts, and light manufacturing zones—locations that already consume a great deal of electricity and stand to benefit quickly from on-site generation.

Add to this the fact that solar adoption across these segments is still lagging behind the city’s potential, and the message becomes clear: Dubai may be a mature market, but its mid-size rooftops remain a wide-open playing field for proactive solar developers.

What’s Changing: A Market in Motion

Dubai was one of the first markets Planno mapped, and we’ve been monitoring it closely for over a year. This long-term view gives us real-time insight into how solar adoption is evolving—and where new growth is emerging.

Between late 2023 and Q1 2025, the number of solar-equipped C&I rooftops grew by 39%, showing that even in a mature market, momentum is far from slowing. The most notable growth came from mid-sized rooftops, especially in the 2,000–4,000 m² range.

Why mid-size? These rooftops hit the sweet spot: large enough to generate savings, yet simple enough to develop quickly. Developers are shifting focus here for faster approvals, better ROI, and shorter sales cycles.

What we’re seeing is a second wave of solar in Dubai—driven not by mega-projects, but by thousands of untapped rooftops hiding in plain sight.

Key Insights & Takeaways

- Dubai still holds 4 GWp of untapped rooftop solar potential

- Mid-sized rooftops (2,000 to 8,000 m²) dominate the market — and adoption here is still low

- Solar adoption rose +39% in just over one year

- Large rooftops remain underutilized and could offer major aggregated capacity

- The next wave of projects will likely come from overlooked warehouses and logistics zones

How Planno Unlocks Rooftop Solar Opportunities

Planno makes this level of rooftop market intelligence actionable. Our platform uses geospatial AI to identify, size, and qualify rooftops for solar in every region — so you don’t have to guess where to go next. We also help you contact building owners and managers directly, turning intelligence into leads.

🚀 Want to explore rooftops in the GCC?

FAQ

What is the rooftop solar potential in Dubai?

Dubai’s C&I rooftops offer a total potential of 5 GWp, with 4 GWp still untapped.

Why is Dubai considered a mature solar market?

DEWA’s Shams Dubai program has supported rooftop solar since 2015, leading to a strong ecosystem of solar providers and thousands of installed systems.

Where is the growth in Dubai’s solar market today?

The biggest growth is now happening in mid-sized rooftops (2,000–8,000 m²), which are abundant and underpenetrated.